As organisations de-risk supply chains and reduce reliance on China, Canada offers a strategic sourcing alternative, if it can overcome capital hurdles

For Chief Procurement Officers and supply chain leaders, the mandate to diversify critical mineral sourcing is no longer just a sustainability goal; it is a strategic imperative.

As geopolitical tensions rise and the race for electrification accelerates, reliance on a single dominant market – specifically China – poses an unacceptable risk to business continuity.

Canada has positioned itself as a viable alternative for Western supply chains, boasting vast geological potential. However, a recent report by the Royal Bank of Canada (RBC) highlights a critical bottleneck.

The nation requires significantly more “patient, risk capital” to transition from potential reserves to a reliable sourcing hub. For procurement leaders, understanding these investment dynamics is essential for long-term category planning.

The demand trajectory

The definition of ‘critical minerals’ varies by jurisdiction, yet the core commodities essential for modern industry – copper, lithium, cobalt and nickel – remain consistent.

For procurement executives in automotive, defence and electronics, securing these materials is becoming increasingly complex.

According to the International Energy Agency (IEA), the critical minerals industry is projected to grow two to three times globally, requiring a capital injection from US$500bn to US$600bn by 2040.

This demand is driven not only by electric vehicle (EV) production but also by the expansion of clean energy infrastructure and defence manufacturing.

While this growth presents a sourcing opportunity, the RBC warns that Canada’s current lack of capital investment threatens its ability to meet this rising demand, potentially leaving buyers with supply deficits.

All sustainability, net zero and sustainable procurement leaders should attend:

- Procurement & Supply Chain LIVE: The Net Zero Summit – QEII Centre, London, March 4-5

- Procurement & Supply Chain LIVE: The US Summit – Navy Pier, Chicago, April 21-22

Co-located with Sustainability LIVE, these events brings together CPOs, CSCO, CSOs, ESG leaders and senior decision-makers at a moment when sustainability, supply chains and commercial performance are increasingly interconnected.

Tickets can be booked online today for The Net Zero Summit and The US Summit. Group discounts available.

Structural barriers to sourcing

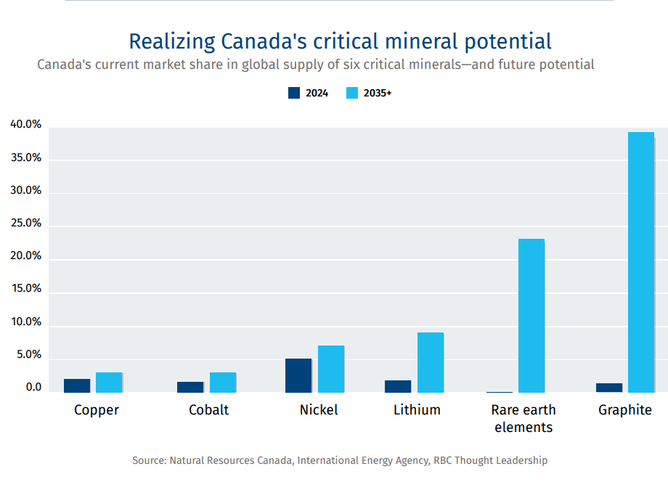

Despite its geological wealth, Canada remains a minor player in the current market, accounting for just 2% of the global supply of six core metals.

The Canadian government aims to increase this to 14% over the next 15 years – a target that relies heavily on closing the investment gap.

For procurement leaders assessing market viability, the historical allocation of capital in Canada is telling.

Over the past 25 years, only 11% of Canada’s mining capital was directed toward critical minerals, compared to 70% for gold and precious metals. In contrast, Australia allocated double that amount to critical materials during the same period.

Furthermore, the downstream supply chain remains a concern. China currently controls 70% of the global refining market share for 19 of the 20 most critical minerals.

Canada faces a refining deficit, possessing only one active copper smelter. For CPOs, this highlights a continued risk: even if raw extraction occurs in Canada, the processing bottleneck may still lead back to dominant Asian markets.

Strategic partnerships and corridors

To mitigate these risks, Canadian entities are attempting to scale capital across the value chain.

The Canada Growth Fund (CGF) has initiated investments in key projects, including Thompson Nickel Mines in Manitoba and Nouveau Monde Graphite in Quebec. However, sovereign commitment alone is insufficient.

The RBC suggests that “mineral corridors” – shared infrastructure for processing and logistics – could improve project economics, making them more attractive to investors and more reliable for buyers.

By clustering regional refining hubs, the industry can reduce logistics costs and improve sustainability metrics.

For North American procurement strategies, the Canada-US relationship is pivotal. With the US government heavily investing in industrial supply chain resilience, a strengthened partnership could position Canada as a primary nearshore supplier.

While maintaining alliances with European and Asian markets remains prudent for diversification, a robust Canada-US mineral corridor offers the most immediate path to supply chain security for Western OEMs.

Procurement Magazine

Leave feedback about this